# Run this command to install the required packages.

# You need to do this only once.

install.packages(

c(

"tidyverse", "broom", "ggdist", "distributional", "gapminder",

"mgcv", "gratia", "gganimate", "gifski"

)

)Visualizing Uncertainty and Trends

Required packages

Install the required packages:

1. Error bars and other uncertainty visualizations

We’ll be working with the gapminder dataset that contains information about life expectancy and GDP per capita for hundreds of countries around the globe.

library(tidyverse)

library(broom) # for extracting regression parameters

library(gapminder) # for dataset

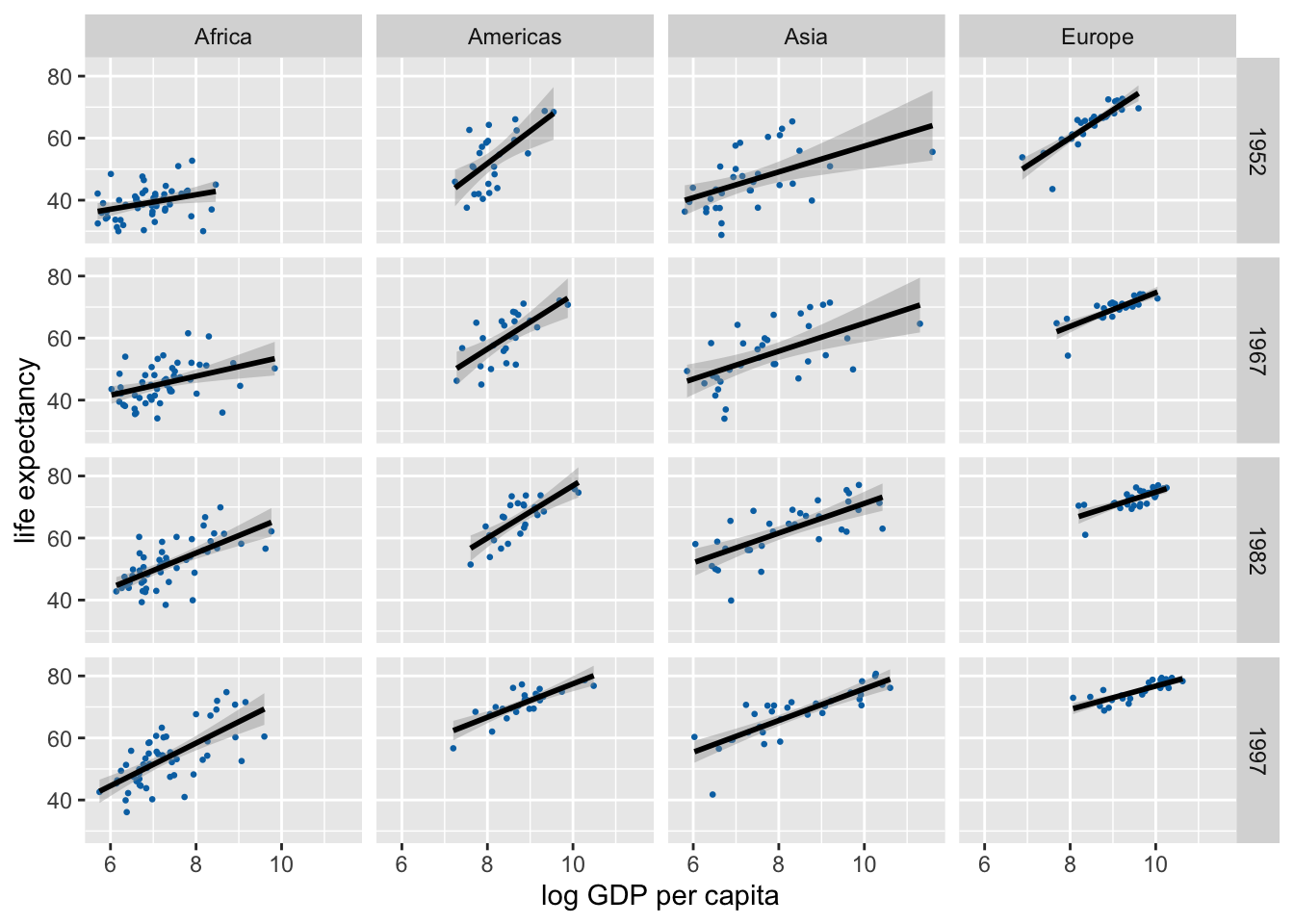

gapminder %>%

filter(

continent != "Oceania",

year %in% c(1952, 1967, 1982, 1997)

) |>

ggplot(aes(log(gdpPercap), lifeExp)) +

geom_point(size = 0.5, color = "#0072B2") +

geom_smooth(method = "lm", formula = y ~ x, color = "black") +

xlab("log GDP per capita") +

scale_y_continuous(

name = "life expectancy",

breaks = c(40, 60, 80)

) +

facet_grid(year ~ continent)

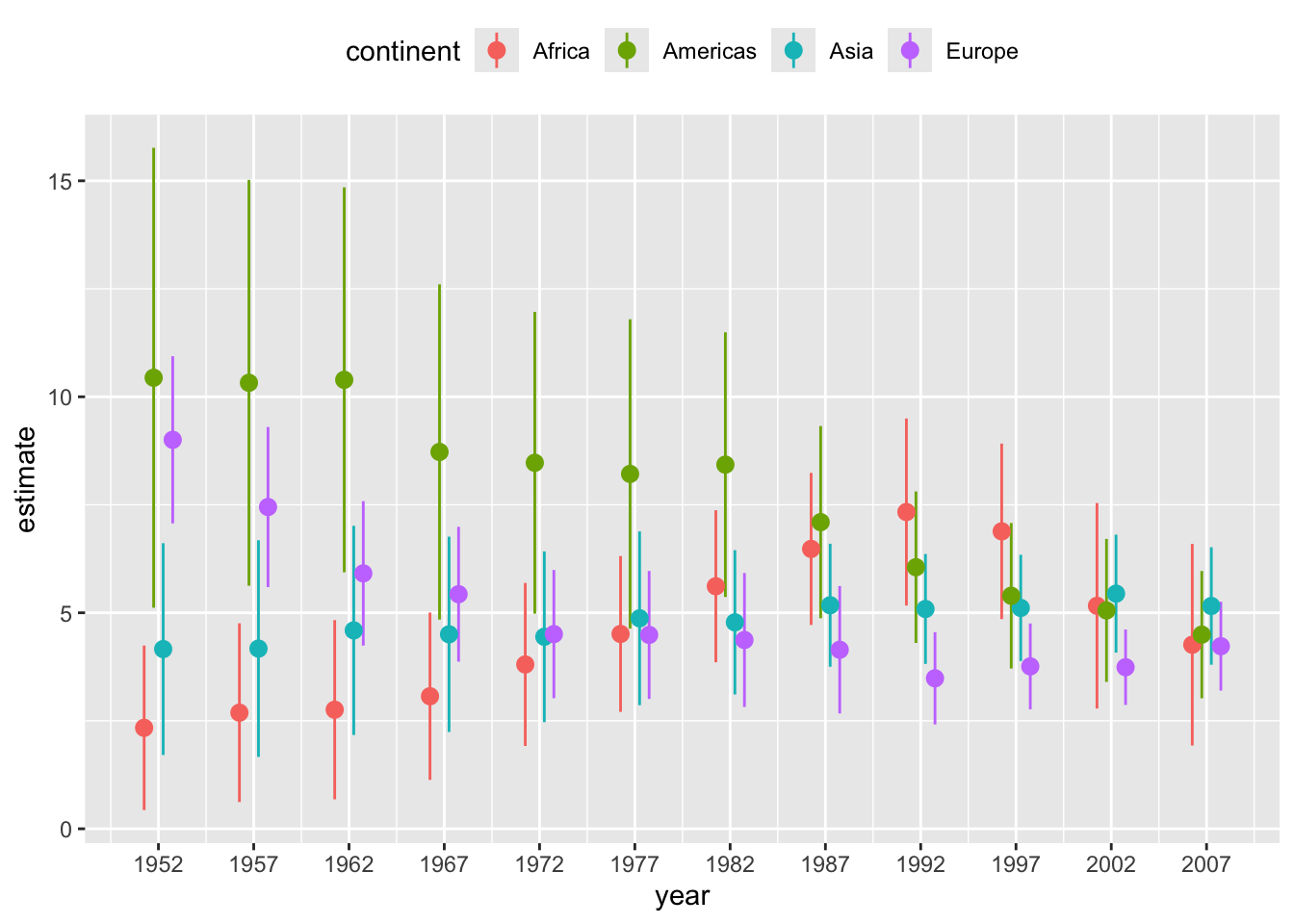

Let’s calculate uncertainties in the regression slopes and then visualize those.

lm_data <- gapminder |>

nest(data = -c(continent, year)) |>

mutate(

fit = map(data, ~lm(lifeExp ~ log(gdpPercap), data = .x)),

tidy_out = map(fit, tidy)

) |>

unnest(cols = tidy_out) |>

select(-data, -fit) |>

filter(term != "(Intercept)", continent != "Oceania")

lm_data# A tibble: 48 × 7

continent year term estimate std.error statistic p.value

<fct> <int> <chr> <dbl> <dbl> <dbl> <dbl>

1 Asia 1952 log(gdpPercap) 4.16 1.25 3.33 0.00228

2 Asia 1957 log(gdpPercap) 4.17 1.28 3.26 0.00271

3 Asia 1962 log(gdpPercap) 4.59 1.24 3.72 0.000794

4 Asia 1967 log(gdpPercap) 4.50 1.15 3.90 0.000477

5 Asia 1972 log(gdpPercap) 4.44 1.01 4.41 0.000116

6 Asia 1977 log(gdpPercap) 4.87 1.03 4.75 0.0000442

7 Asia 1982 log(gdpPercap) 4.78 0.852 5.61 0.00000377

8 Asia 1987 log(gdpPercap) 5.17 0.727 7.12 0.0000000531

9 Asia 1992 log(gdpPercap) 5.09 0.649 7.84 0.00000000760

10 Asia 1997 log(gdpPercap) 5.11 0.628 8.15 0.00000000335

# ℹ 38 more rowsIn standard ggplot we have to calculate and draw error bars manually.

ggplot(lm_data) +

aes(

x = year, y = estimate,

ymin = estimate - 1.96*std.error,

ymax = estimate + 1.96*std.error,

color = continent

) +

geom_pointrange(

position = position_dodge(width = 2)

) +

scale_x_continuous(

breaks = unique(gapminder$year)

) +

theme(legend.position = "top")

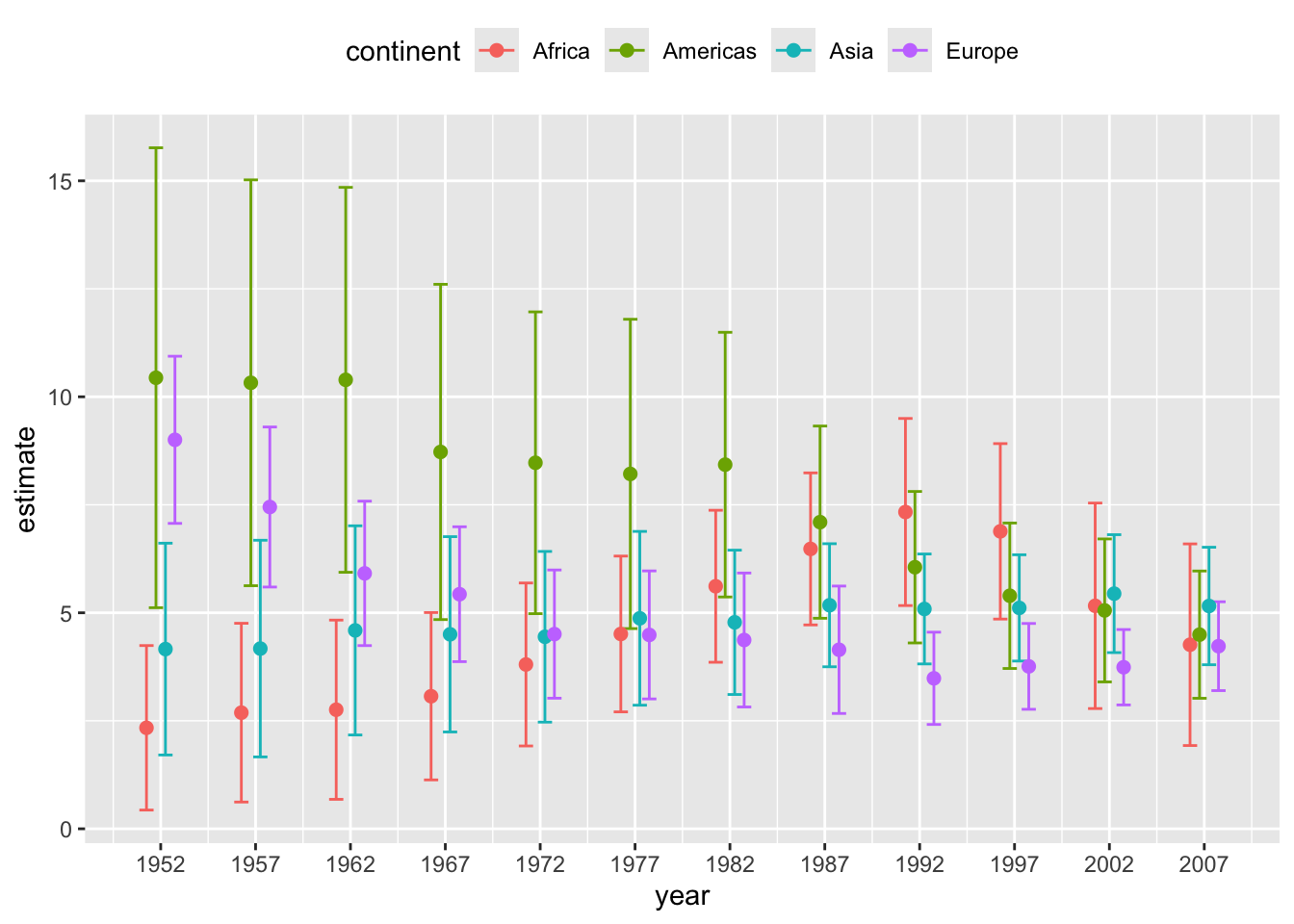

# alternative version with error bars with caps

ggplot(lm_data) +

aes(

x = year, y = estimate,

ymin = estimate - 1.96*std.error,

ymax = estimate + 1.96*std.error,

color = continent

) +

geom_errorbar(

position = position_dodge(width = 2),

width = 3 # cap width

) +

geom_point( # geom_errorbar() doesn't draw the point estimate

position = position_dodge(width = 2),

size = 2

) +

scale_x_continuous(

breaks = unique(gapminder$year)

) +

theme(legend.position = "top")

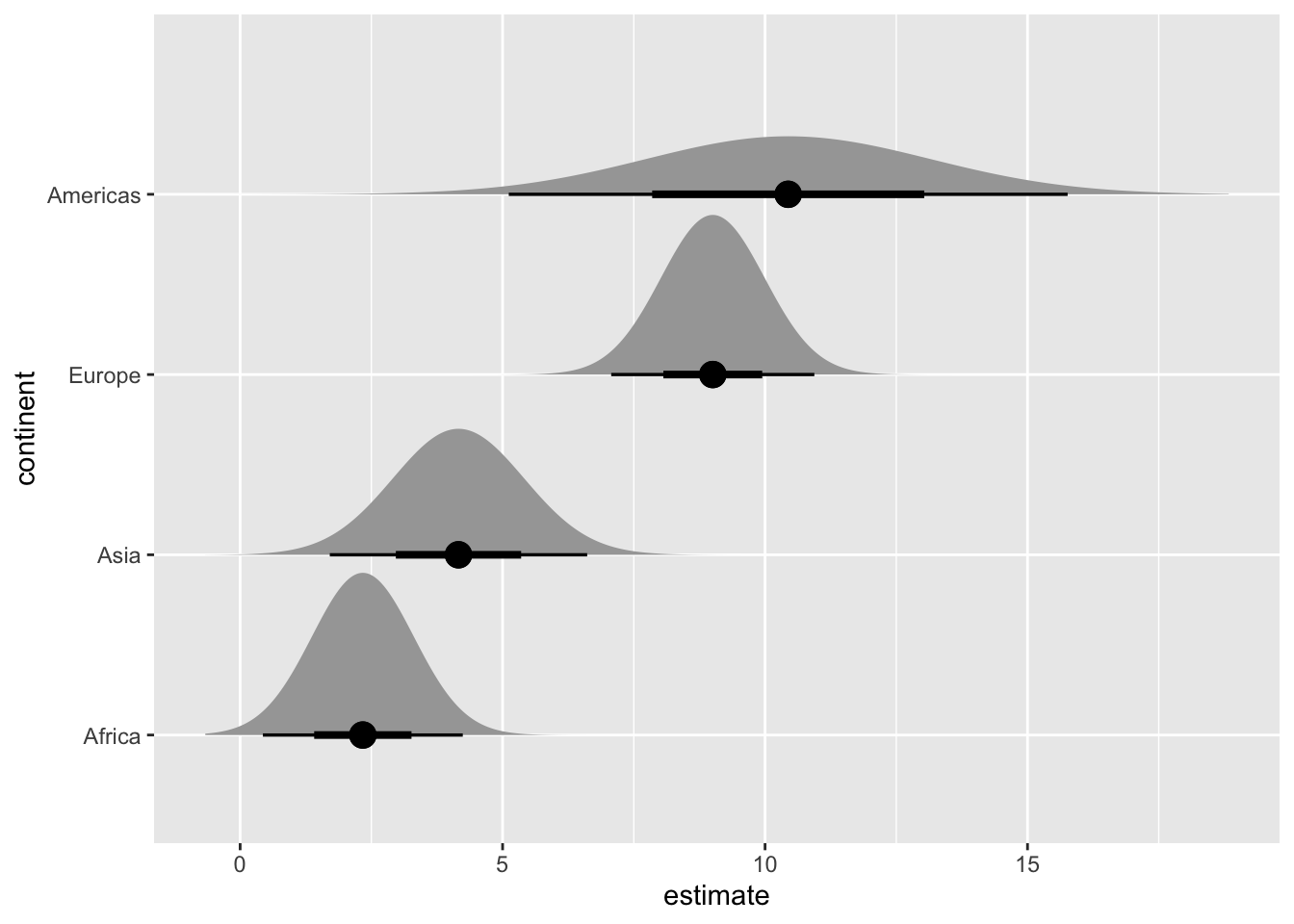

We can create many more uncertainty visualizations with the ggdist package.

library(ggdist)

library(distributional) # for dist_normal()

# subset to year 1952 only

lm_data_1952 <- lm_data |>

filter(year == 1952) |>

mutate(

continent =

fct_reorder(continent, estimate)

)

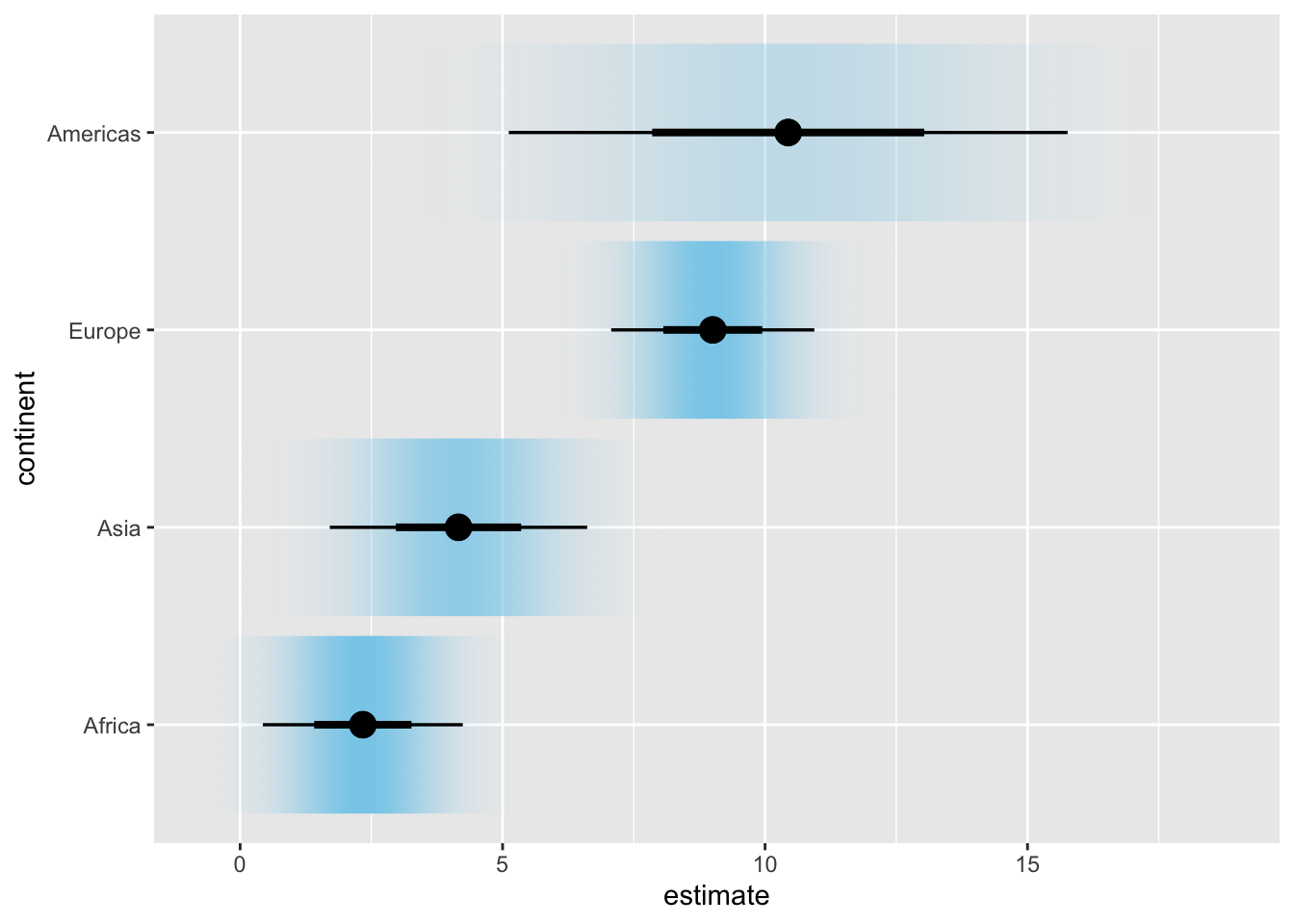

# half eyes

ggplot(lm_data_1952, aes(x = estimate, y = continent)) +

stat_halfeye(

aes(dist = dist_normal(

mu = estimate, sigma = std.error

)),

point_size = 4

)

# confidence strips

ggplot(lm_data_1952, aes(x = estimate, y = continent)) +

stat_gradientinterval(

aes(dist = dist_normal(

mu = estimate, sigma = std.error

)),

point_size = 4,

fill = "skyblue"

)

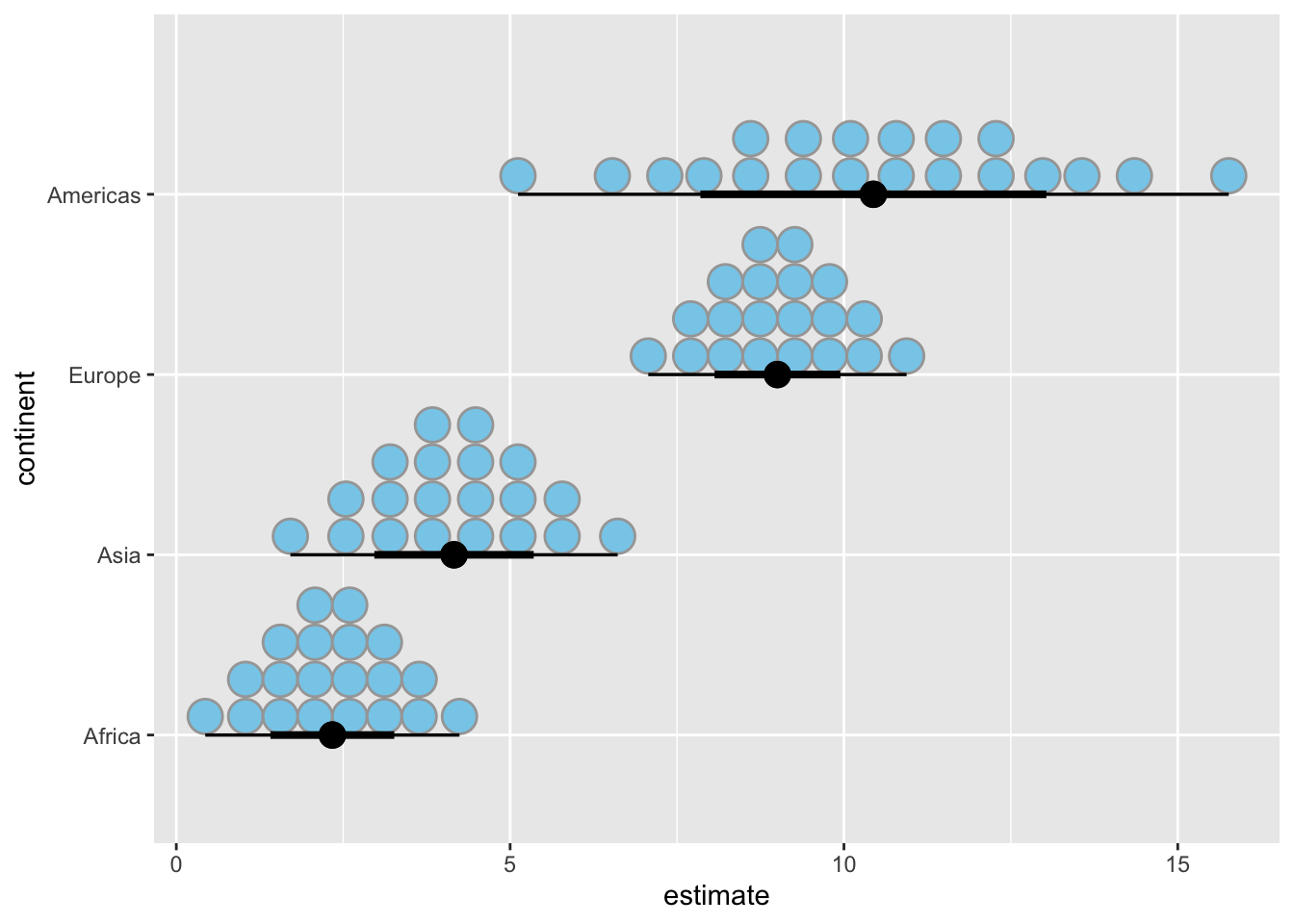

# quantile dotplot

ggplot(lm_data_1952, aes(x = estimate, y = continent)) +

stat_dotsinterval(

aes(dist = dist_normal(

mu = estimate, sigma = std.error

)),

point_size = 4,

fill = "skyblue",

quantiles = 20

)

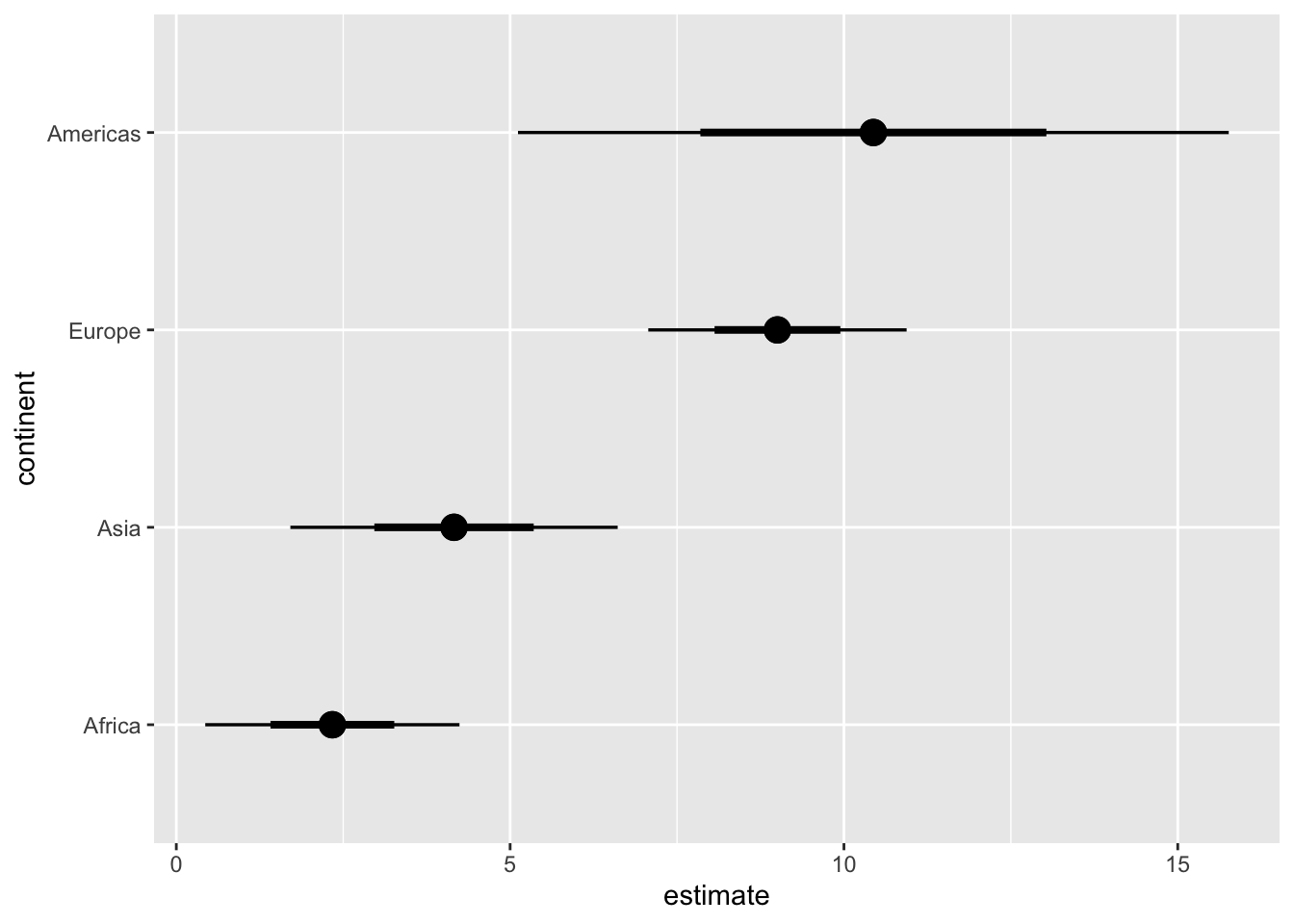

# regular errorbars

ggplot(lm_data_1952, aes(x = estimate, y = continent)) +

stat_pointinterval(

aes(dist = dist_normal(

mu = estimate, sigma = std.error

)),

point_size = 4

)

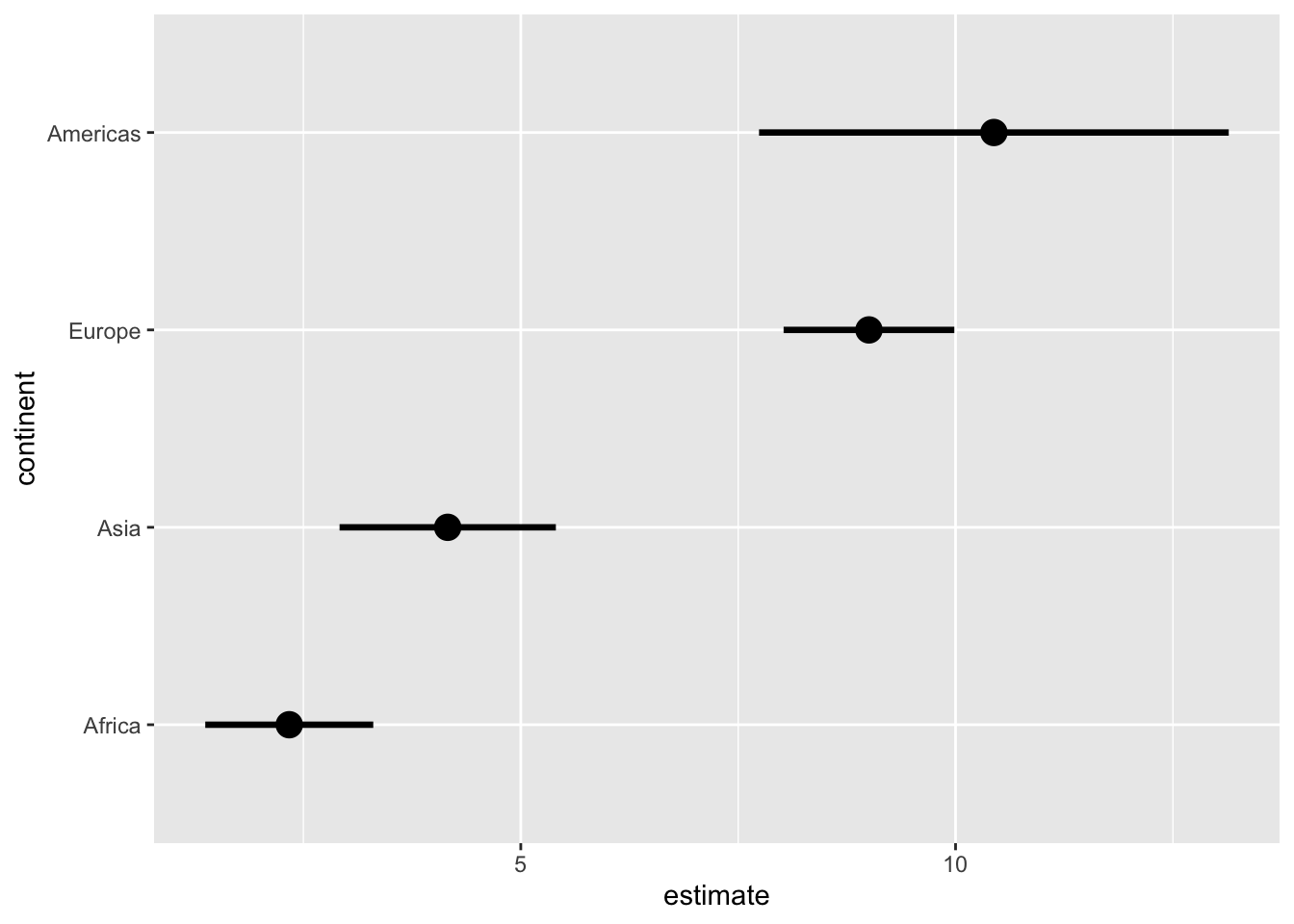

# use .width to customize the error intervals shown

ggplot(lm_data_1952, aes(x = estimate, y = continent)) +

stat_pointinterval(

aes(dist = dist_normal(

mu = estimate, sigma = std.error

)),

point_size = 4,

#.width = c(.68, .95, .997) # 1, 2, 3 SD

.width = .68 # 1 SD only

)

Exercises

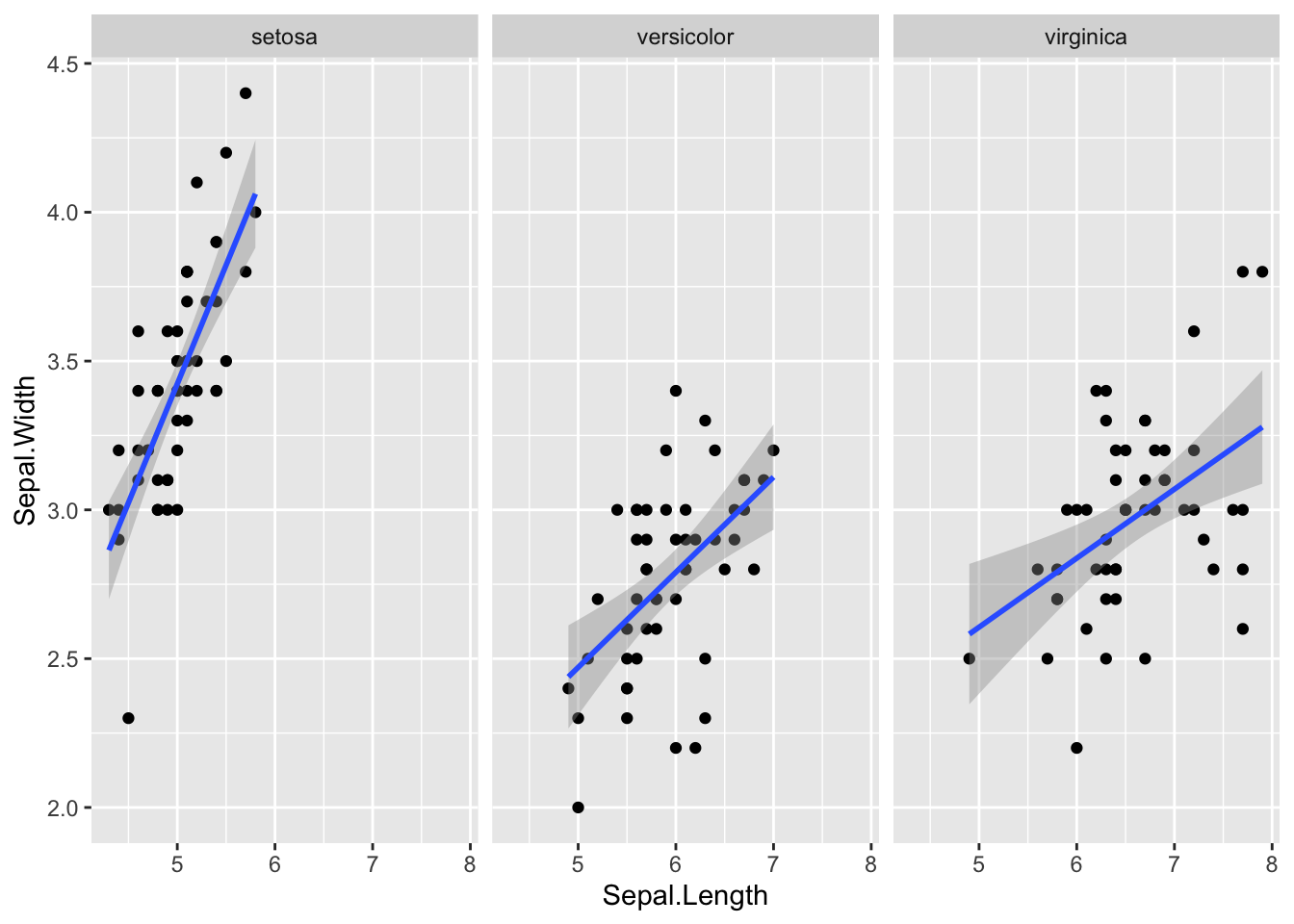

Visualize the uncertainty in the regression slopes for the iris dataset.

ggplot(iris, aes(Sepal.Length, Sepal.Width)) +

geom_point() +

geom_smooth(method = "lm", formula = y ~ x) +

facet_wrap(~Species, nrow = 1)

# your code here2. Hypothetical Outcome Plots

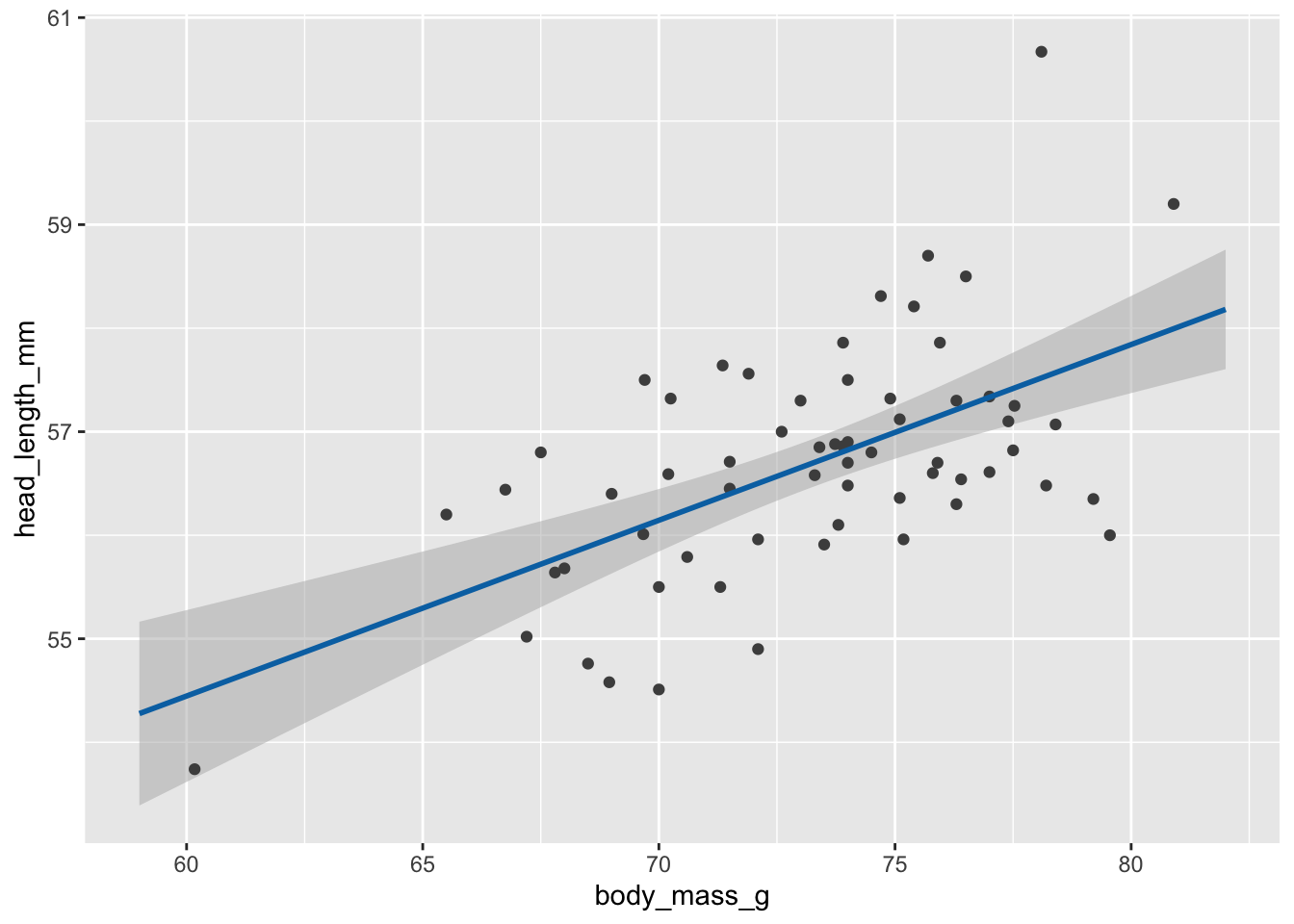

We’ll be working with the blue jays dataset which contains various body size measurements of blue jays birds. Specifically we’ll be looking at the relationship between the head length and the body mass, which we can model with a linear regression. We want to display the uncertainty in this regression line with an animated hypothetical outcomes plot.

Step 1: Fit a linear model and extract samples from the fitted model.

library(mgcv) # to fit generalized additive models with gam()

library(gratia) # to generate samples from fitted model

# read in data

blue_jays <- read_csv(

"https://wilkelab.org/dataviz_shortcourse/datasets/blue_jays.csv",

show_col_types = FALSE

)

# subset to male birds only

blue_jays_male <- blue_jays |>

filter(sex == "M")

# fit a linear model

# need to use gam() so we can take advantage of the functions provided by gratia

fit <- gam(head_length_mm ~ body_mass_g, data = blue_jays_male, method = "REML")

# new data table with x values only, for model prediction

blue_jays_new <- tibble(

body_mass_g = seq(from = 59, to = 82, length.out = 100)

) |>

mutate(.row = row_number()) # needed to join in fitted samples

# fitted_values() returns mean and confidence band

fv <- fitted_values(fit, data = blue_jays_new)

# fitted_samples() returns independent samples from the fitted model

fs <- fitted_samples(fit, data = blue_jays_new, n = 30, seed = 10) |>

left_join(blue_jays_new, by = ".row")

# static plot with mean and confidence band

ggplot(blue_jays_male, aes(body_mass_g)) +

geom_ribbon(

data = fv, aes(ymin = .lower_ci, ymax = .upper_ci),

fill="grey70", color = NA, alpha = 1/2

) +

geom_point(aes(y = head_length_mm), color = "grey30", size = 1.5) +

geom_line(

data = fv, aes(y = .fitted),

color = "#0072B2", linewidth = 1

)

# static plot with fitted samples

ggplot(blue_jays_male, aes(body_mass_g)) +

geom_ribbon(

data = fv, aes(ymin = .lower_ci, ymax = .upper_ci),

fill="grey70", color = NA, alpha = 1/2

) +

geom_point(aes(y = head_length_mm), color = "grey30", size = 1.5) +

geom_line(

data = fs,

aes(y = .fitted, group = .draw),

color = "#0072B2", linewidth = 0.3

)

Step 2: Make animations with gganimate.

library(gganimate) # to make animations

anim_obj <- ggplot(blue_jays_male, aes(body_mass_g)) +

geom_ribbon(

data = fv, aes(ymin = .lower_ci, ymax = .upper_ci),

fill="grey70", color = NA, alpha = 1/2

) +

geom_point(aes(y = head_length_mm), color = "grey30", size = 1.5) +

geom_line(

data = fs,

aes(y = .fitted, group = .draw),

color = "#0072B2", linewidth = 0.3

) +

transition_manual(.draw) # this is the only change needed to create an animation

# printing the anim object is sufficient to create the animation

anim_obj`nframes` and `fps` adjusted to match transition

In practice we may want to customize how exactly the animation is rendered, such as the exact width/height, number of frames, frames per seconds shown, etc.

animate(

anim_obj,

fps = 5, # frames per second

width = 5.5*100, height = (3/4)*5.5*100, # width and height in pixels

res = 100 # resolution (dots per inch)

)We can save as gif or mp4 with anim_save().

anim_save(

"blue-jays-HOP.gif",

anim_obj,

fps = 5,

width = 5.5*300, height = (3/4)*5.5*300,

res = 300

)Exercises

Visualize the fitted model in this plot of fuel efficiency versus displacement as a hypothetical outcome plot. Note that the fitted model here is y ~ s(x, bs = "cs"). (This is the default formula that geom_smooth() uses when fitting generalized additive models, which it does by default for data sets with 1000 points or more.)

ggplot(mtcars, aes(x = disp, y = mpg)) +

geom_smooth(method = "gam", formula = y ~ s(x, bs = "cs")) +

geom_point(color = "grey30")

# your code here3. Trendlines and de-trending

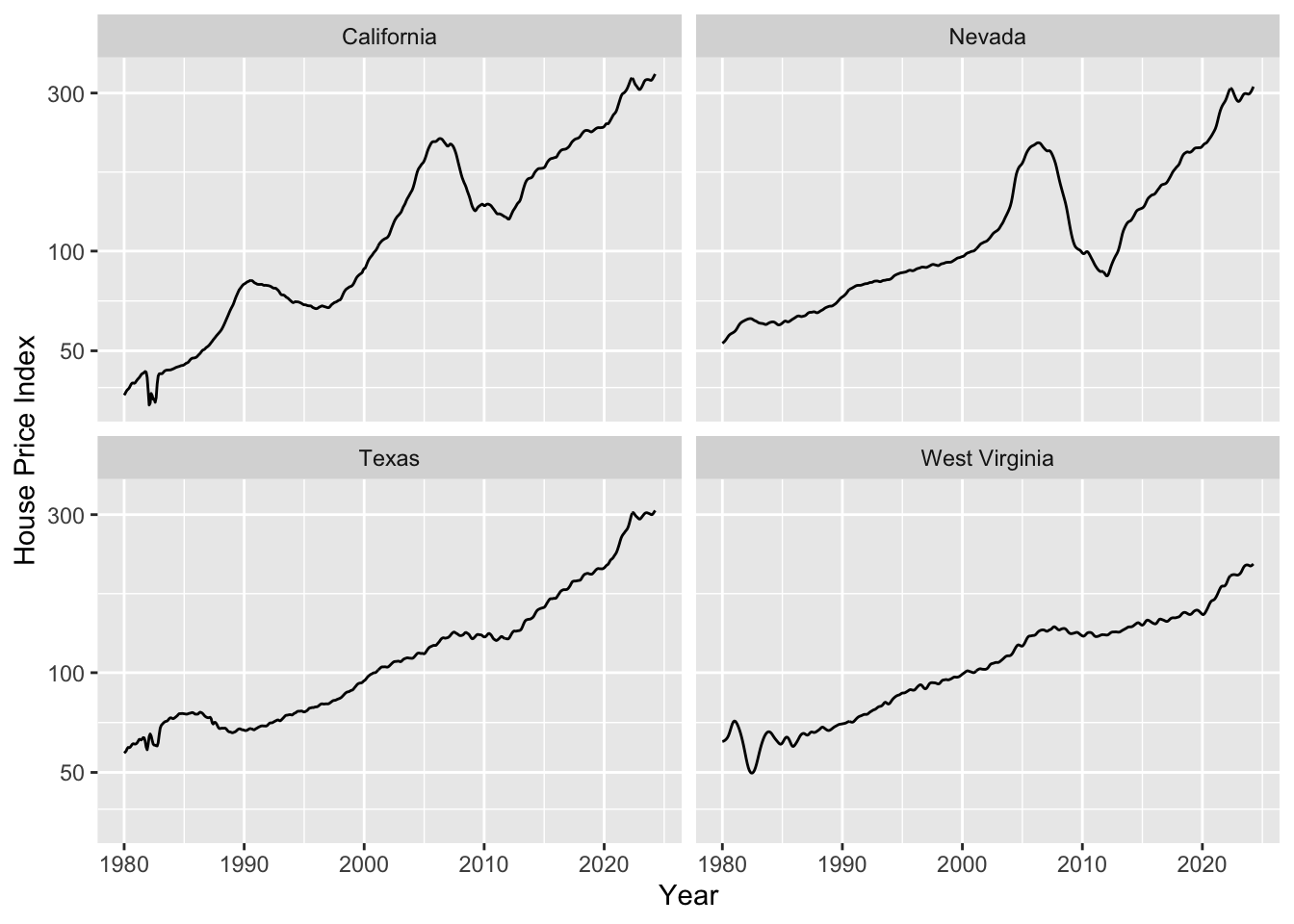

The first example will be trends in the US housing market by state.

# Freddie Mac House Price Index data

# from: https://www.freddiemac.com/research/indices/house-price-index

fmhpi <- read_csv(

"https://wilkelab.org/dataviz_shortcourse/datasets/fmhpi.csv",

show_col_types = FALSE

) |>

filter(year >= 1980) # trends are weird before 1980

# plot house price index (HPI) for a few states

fmhpi |>

filter(state %in% c("California", "Nevada", "West Virginia", "Texas")) |>

ggplot(aes(date_dec, hpi)) +

geom_line() +

xlab("Year") +

scale_y_log10(name = "House Price Index") +

facet_wrap(~state)

As housing prices are growing exponentially, we need to fit a trend line in log space. Let’s do this and plot.

# we fit trendlines separately for all states

fmhpi_trends <- fmhpi |>

nest(data = -state) |>

mutate(

# fit in log space (never fit exponentials in linear space!)

fit_log = map(data, ~lm(log(hpi) ~ date_dec, data = .x)),

# predict long-term trend from fitted model

hpi_trend_log = map2(fit_log, data, ~exp(predict(.x, .y)))

) |>

select(-fit_log) |>

unnest(cols = c(data, hpi_trend_log))

fmhpi_trends |>

filter(state %in% c("California", "Nevada", "West Virginia", "Texas")) |>

ggplot(aes(date_dec, hpi)) +

geom_line(aes(color = "Raw HPI")) +

geom_line(aes(y = hpi_trend_log, color = "trendline")) +

xlab("Year") +

scale_y_log10(name = "House Price Index (HPI)") +

scale_color_manual(

name = NULL,

values = c("Raw HPI" = "#0072B2", trendline = "#D55E00")

) +

facet_wrap(~state) +

theme(legend.position = "bottom")

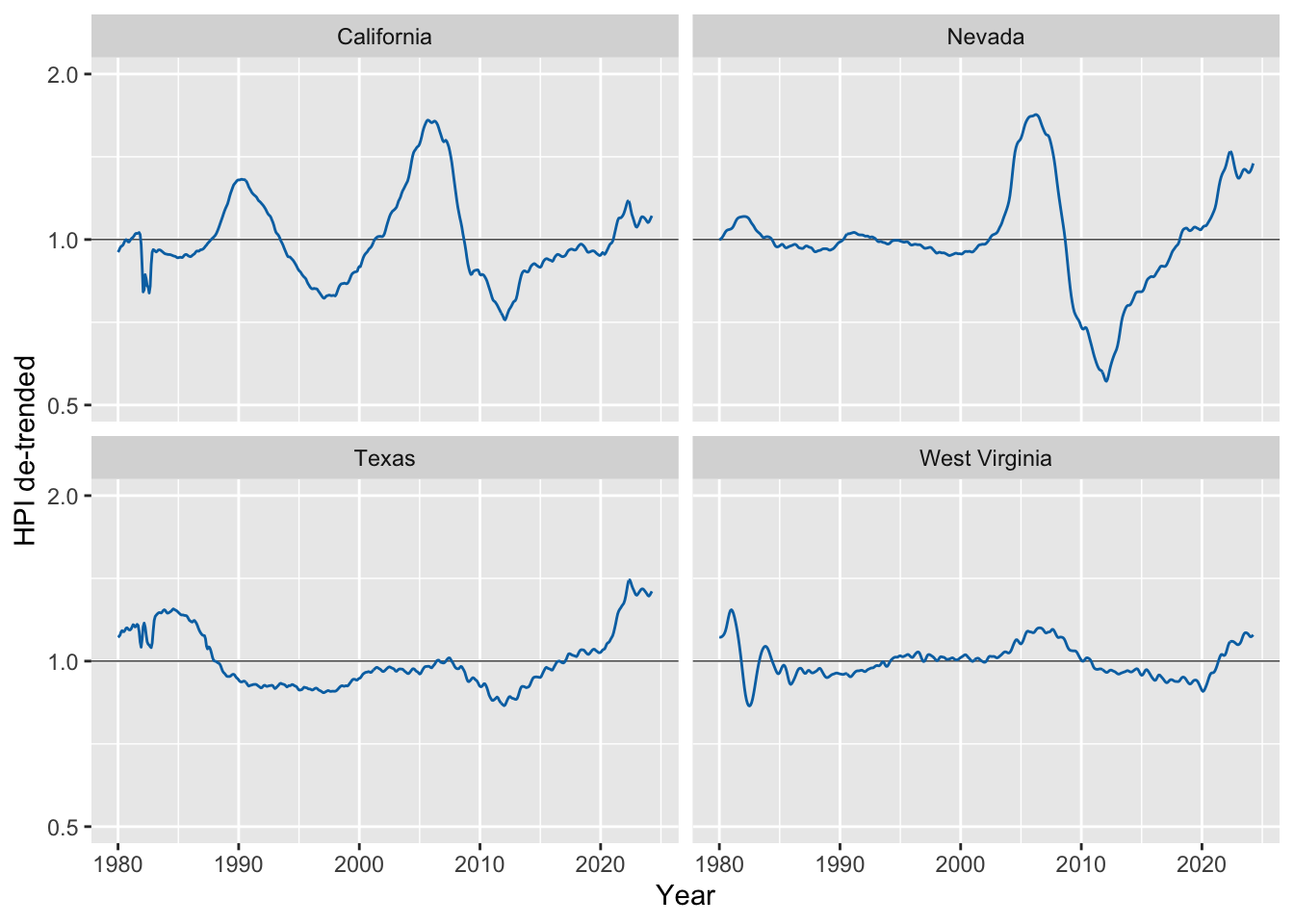

Now we can de-trend by dividing the raw value by the trendline.

fmhpi_trends |>

filter(state %in% c("California", "Nevada", "West Virginia", "Texas")) |>

ggplot(aes(date_dec, hpi/hpi_trend_log)) +

geom_hline(yintercept = 1, linewidth = 0.2) +

geom_line(color = "#0072B2") +

xlab("Year") +

scale_y_log10( # important, still need to use log scale

name = "HPI de-trended",

limits = c(0.5, 2)

) +

facet_wrap(~state)

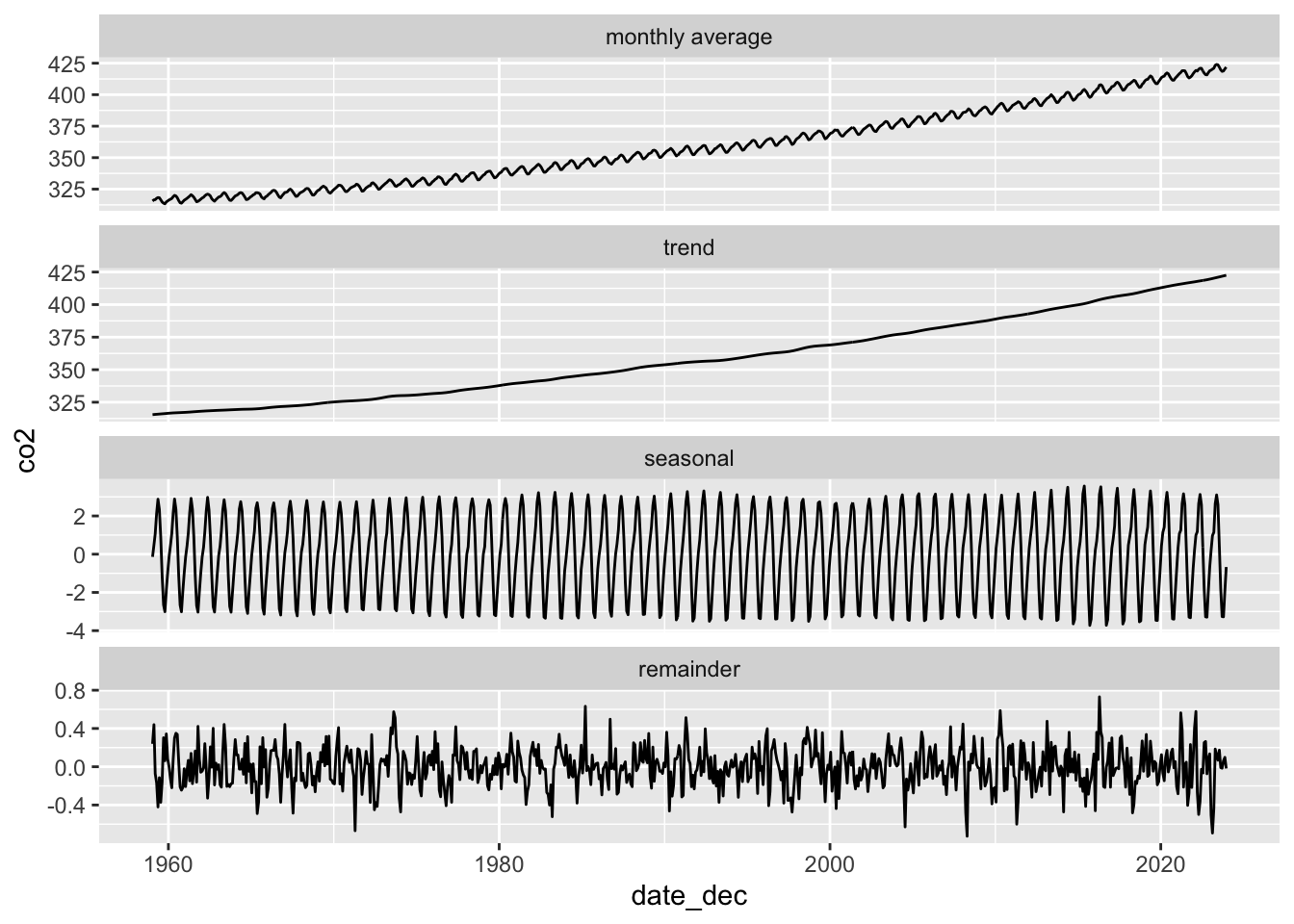

In the second example we will be decomposing monthly CO2 readings into the long-term trend, seasonal fluctuations, and the remainder.

# read in the data

co2 <- read_csv(

"https://wilkelab.org/dataviz_shortcourse/datasets/co2.csv",

show_col_types = FALSE

)

# use complete years only

start_year <- 1959

end_year <- 2023

co2_reduced <- filter(co2, year >= start_year & year <= end_year)

# convert data to time series object

response <- co2_reduced$co2_ave

co2_ts <- ts(

data = response,

start = start_year,

end = c(end_year, 12),

frequency = 12 # we have 12 time points per year

)

# perform STL analysis (Seasonal Decomposition of Time Series by Loess)

co2_stl <- stl(co2_ts, s.window = 7)

# extract components and put together into one table

co2_detrended <- tibble(

date_dec = co2_reduced$date_dec,

response,

seasonal = t(co2_stl$time.series)[1, ],

trend = t(co2_stl$time.series)[2, ],

remainder = t(co2_stl$time.series)[3, ]

)

# plot

co2_detrended |>

rename("monthly average" = response) |>

pivot_longer(-date_dec, names_to = "component", values_to = "co2") |>

mutate(

component = fct_relevel(component, "monthly average", "trend", "seasonal", "remainder")

) |>

ggplot(aes(date_dec, co2)) +

geom_line() +

facet_wrap(~component, scales = "free_y", ncol = 1)

Exercises

Exercises for the HPI data:

Make plots of raw and de-trended HPI data for other US states. Can you find interesting patterns?

Perform a linear (as opposed to logarithmic) de-trending and see how the results differ.

# your code hereExercise for seasonal decomposition: Perform STL analysis on both temperature and precipitation data for Austin, TX. Explore different time ranges for your analysis. What trends are you seeing? Do you think the decomposition works for precipitation data?

# monthly temperature and precipitation data for Austin, TX

atx_temps <- read_csv(

"https://wilkelab.org/dataviz_shortcourse/datasets/atx_temps.csv",

show_col_types = FALSE

)

# pick a range of years to analyze; the earliest complete year is 1939

# and the latest complete year is 2023.

start_year <- 1970

end_year <- 2010

temps_reduced <- filter(atx_temps, year >= start_year & year <= end_year)

# perform the analysis both for average temperature and for precipitation

response <- temps_reduced$temp_ave

# response <- temps_reduced$precip# continue here ...4. Fitting different types of smoothers

When fitting non-linear smoothers to data via geom_smooth(), there are extensive options to customize the smoother and as a result to get quite different fits. Most people just use the geom defaults, but you should be aware that there are customization options and that they substantially affect what you get.

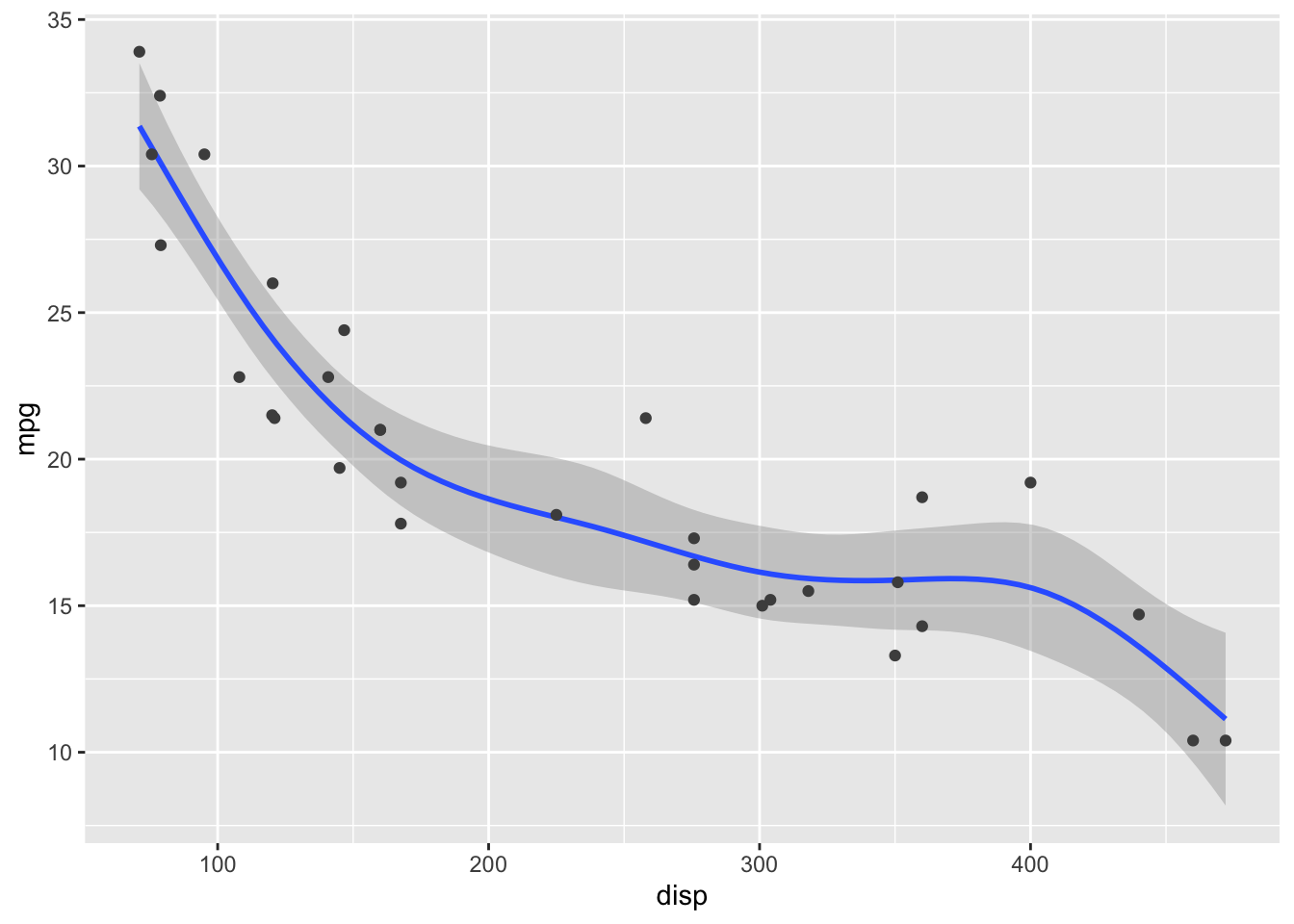

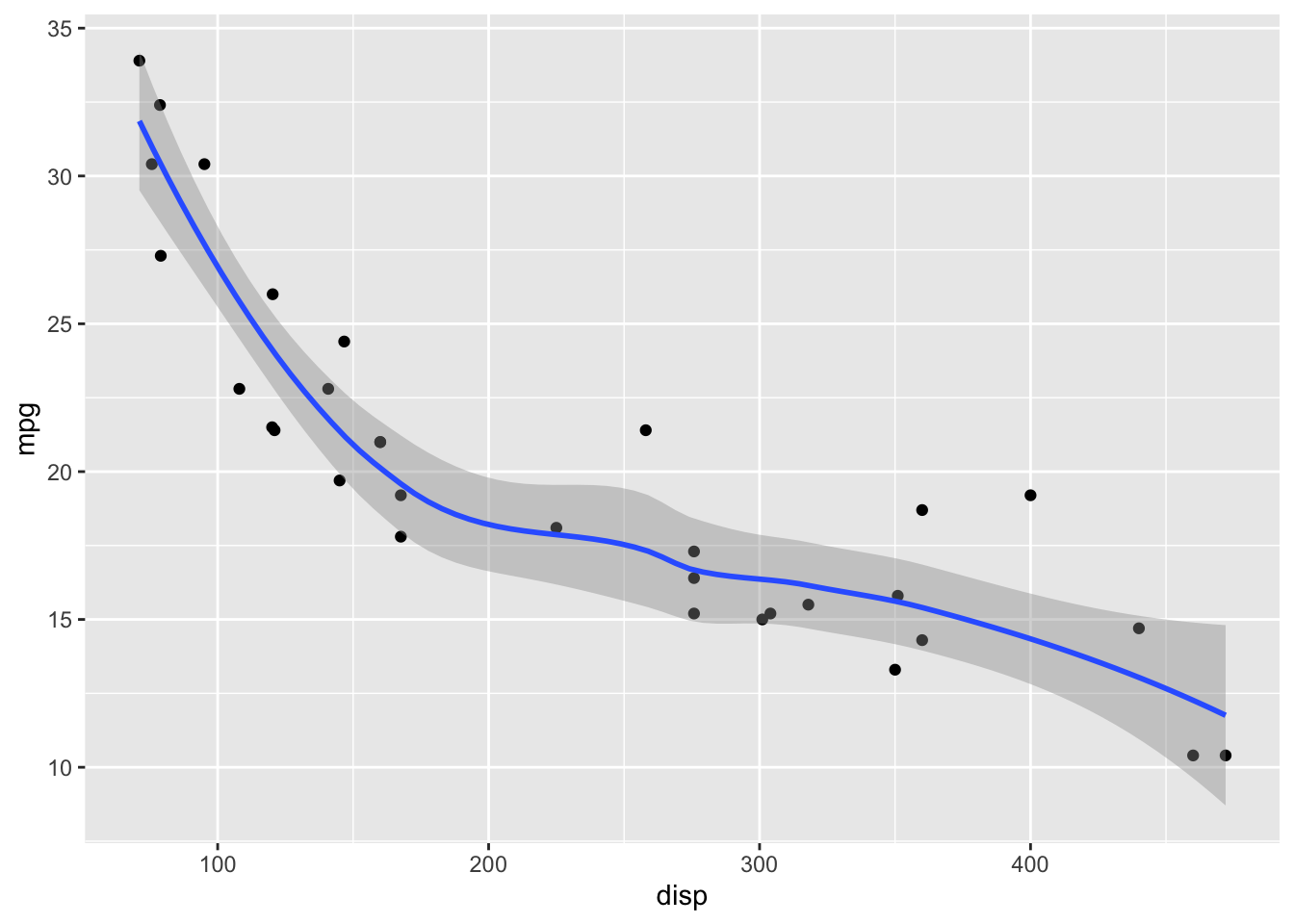

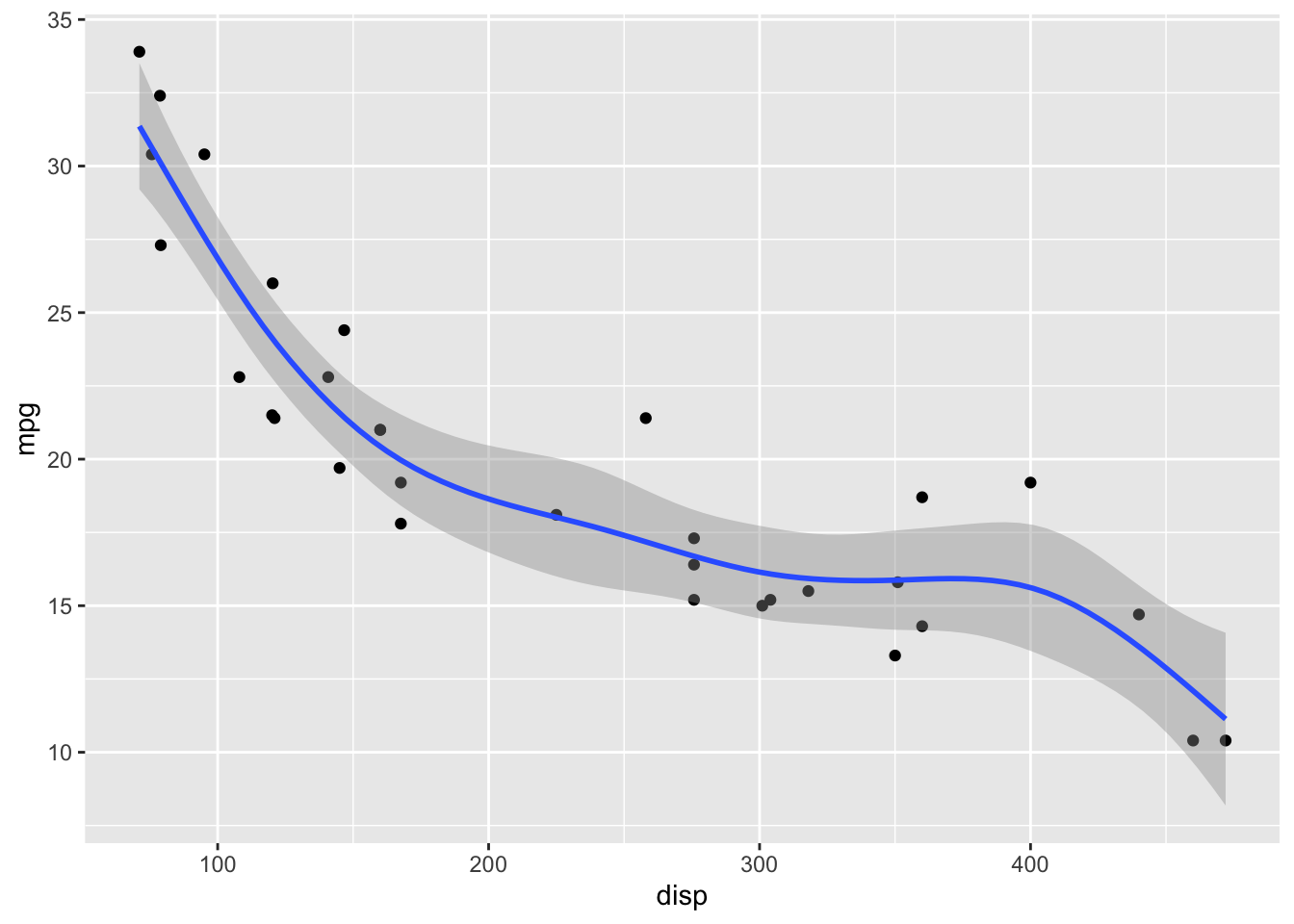

Let’s start with the default options. For small datasets (<1000 data points), geom_smooth() uses LOESS.

ggplot(mtcars) +

aes(disp, mpg) +

geom_point() +

# default for small datasets: loess smoothing

geom_smooth()`geom_smooth()` using method = 'loess' and formula = 'y ~ x'

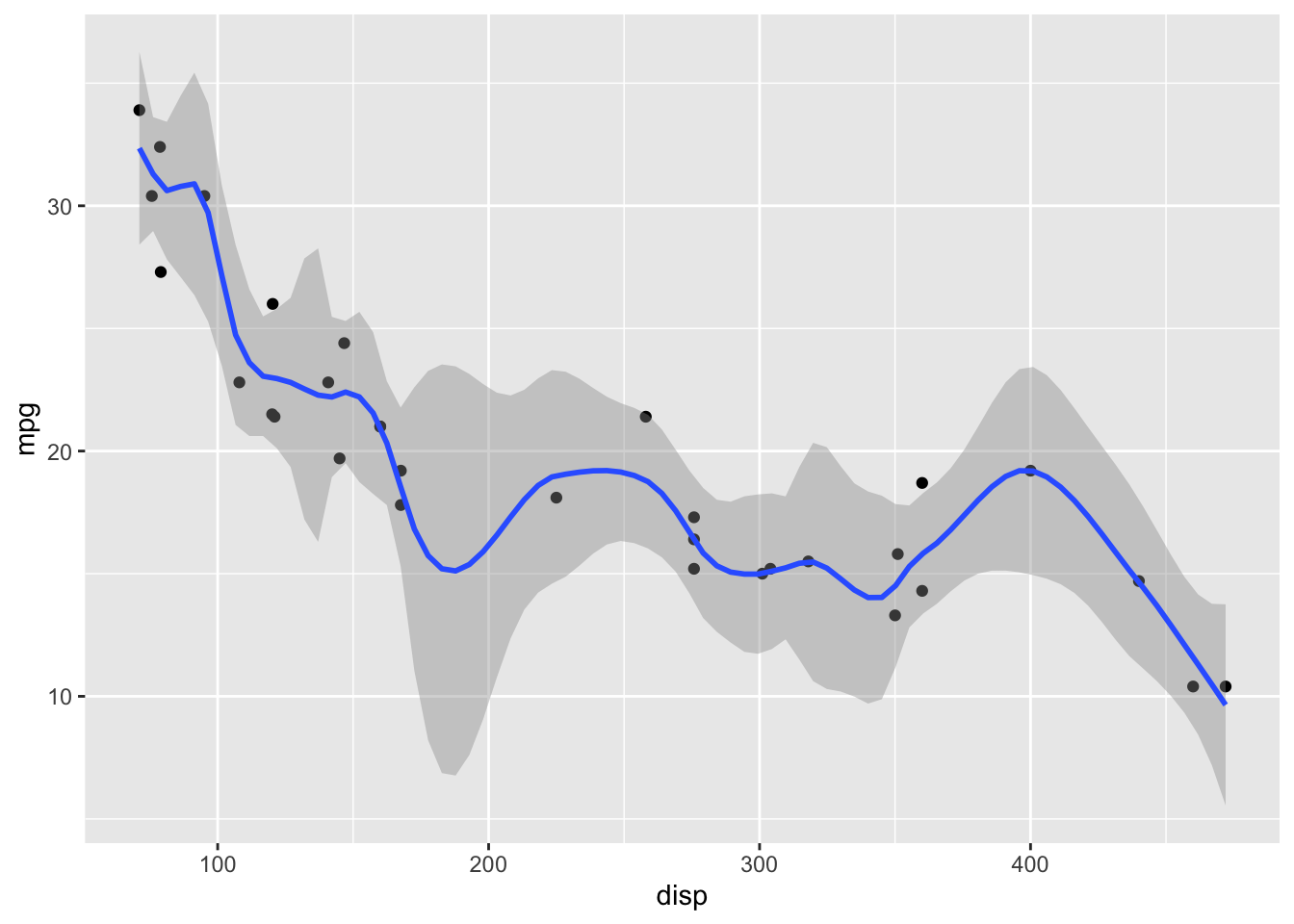

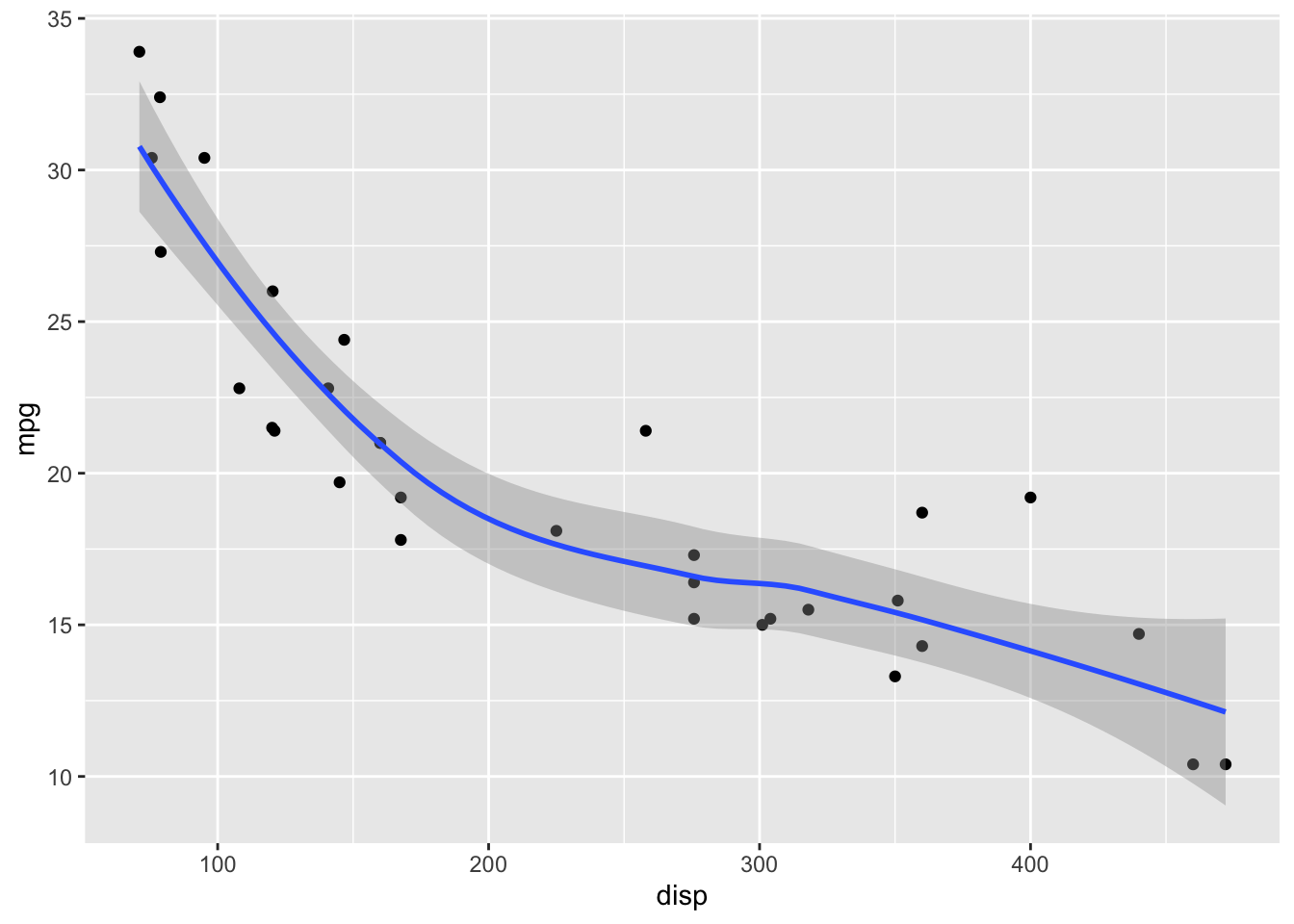

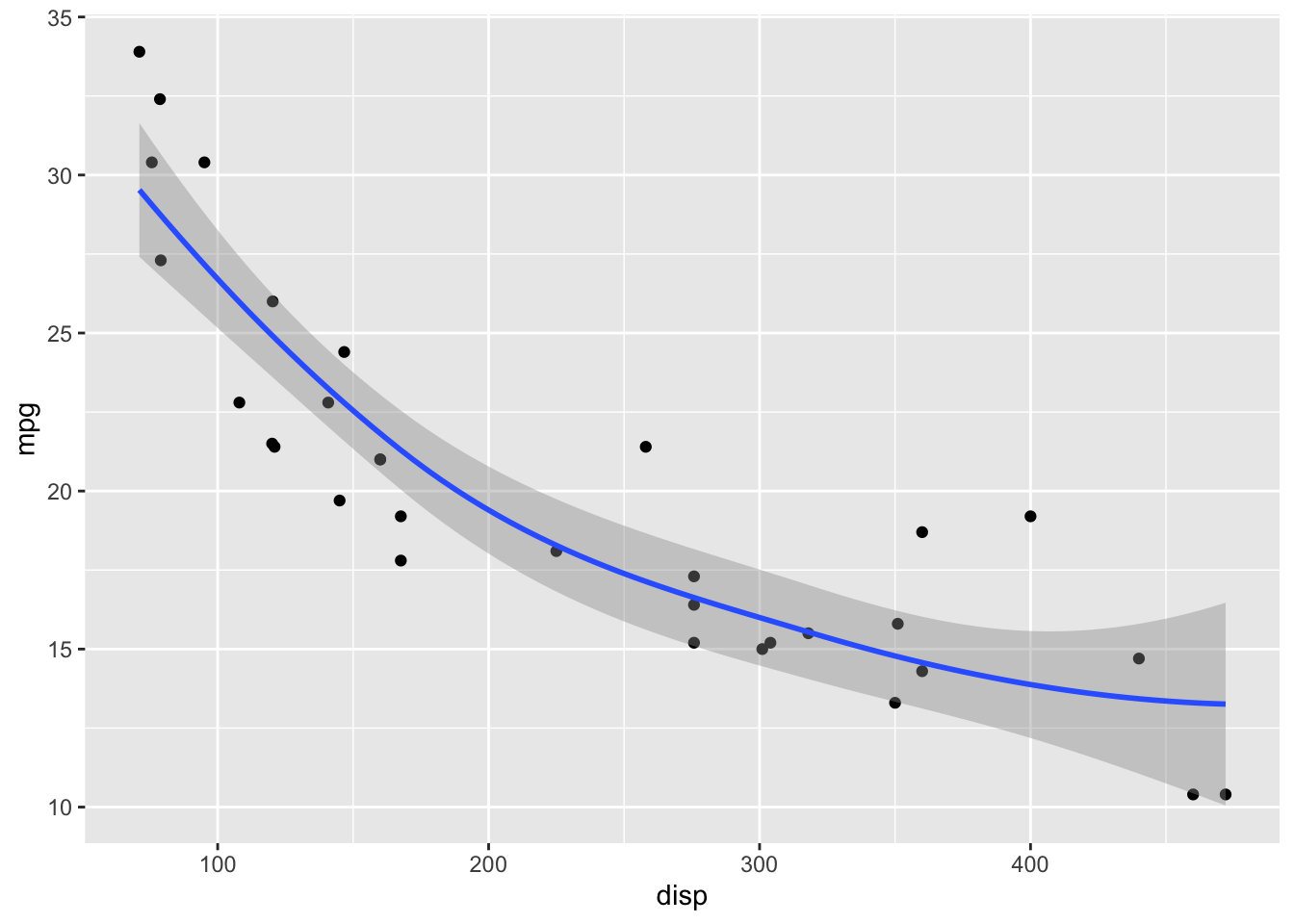

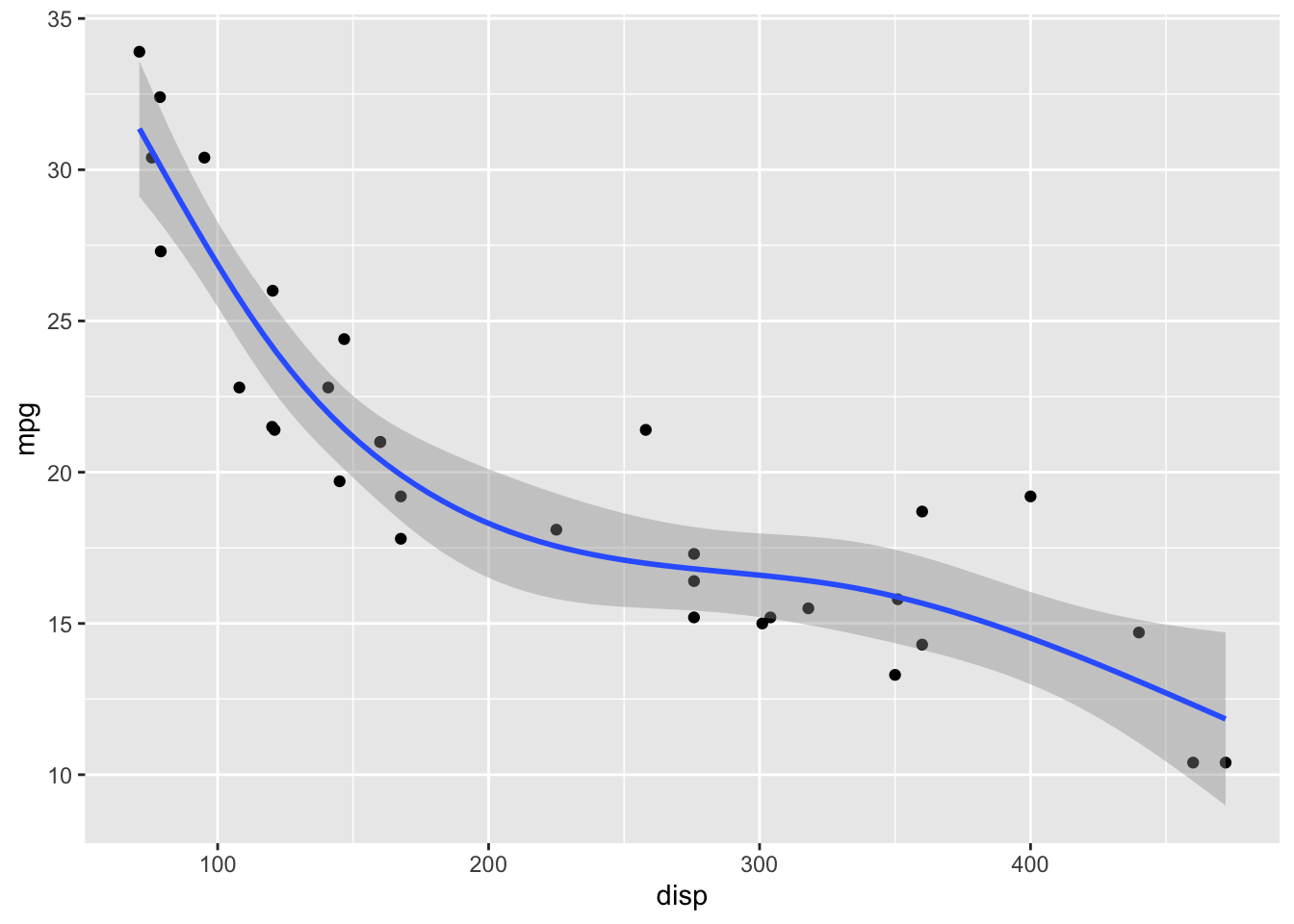

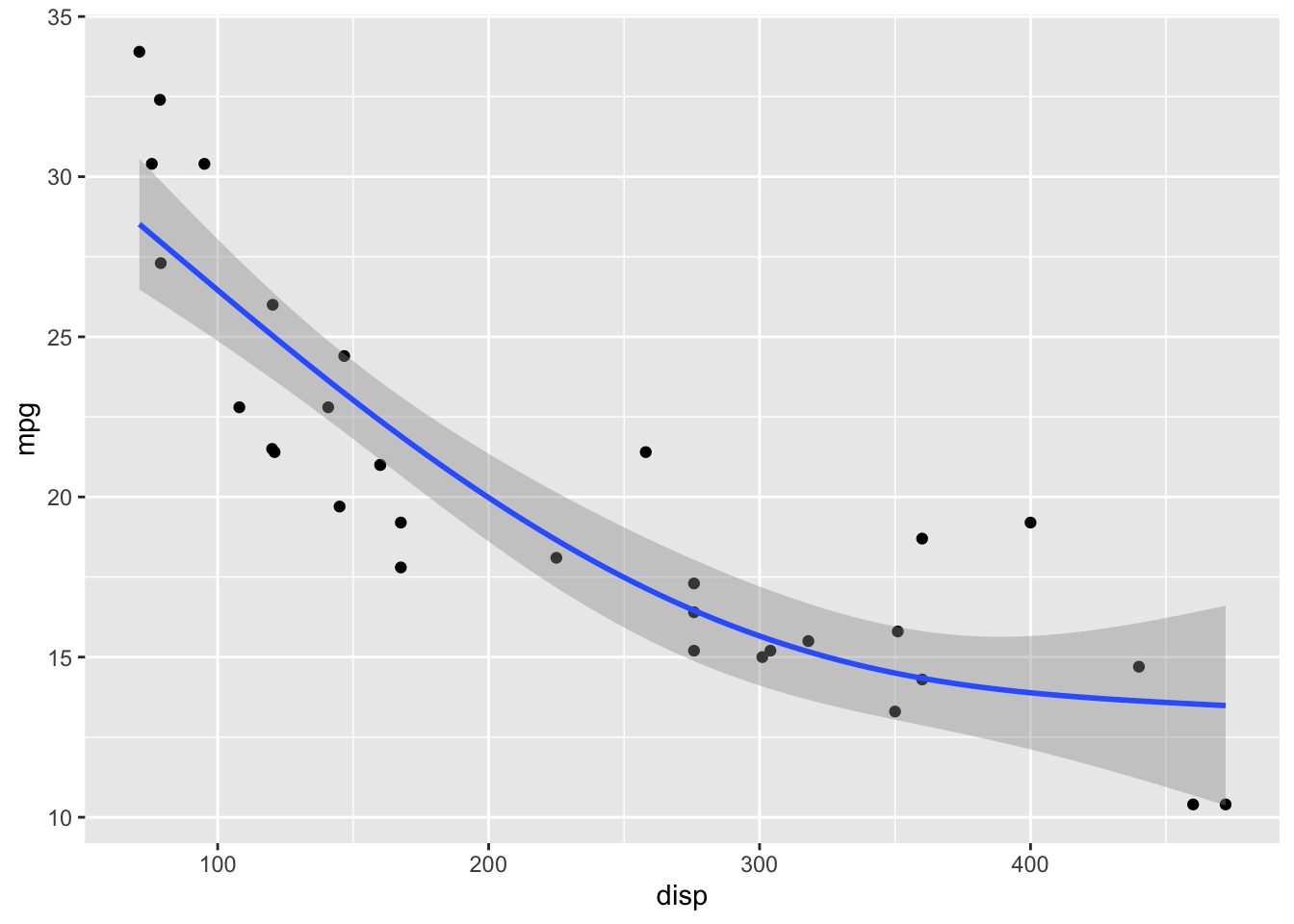

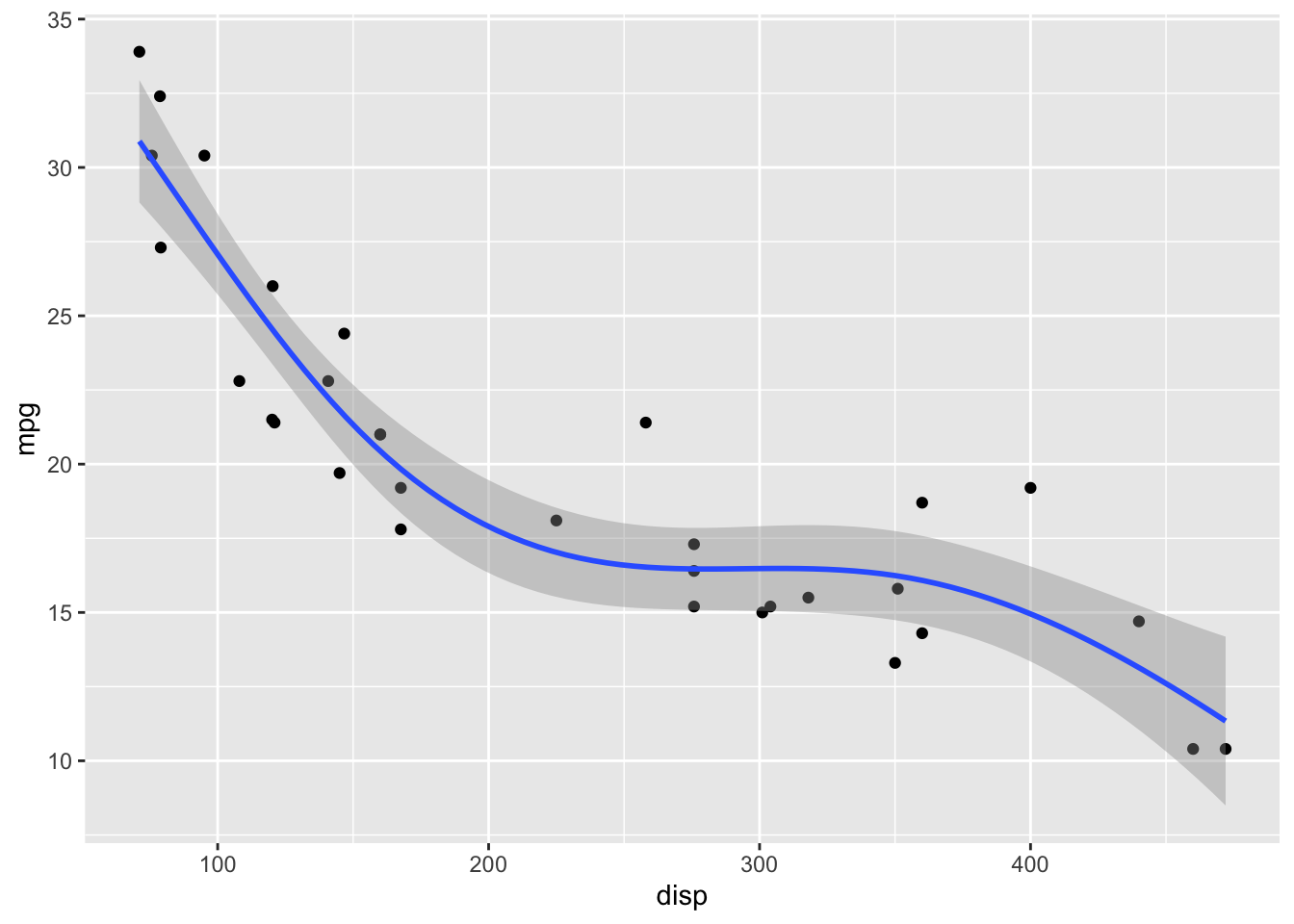

LOESS has a parameter span that determines how smooth the fit will be. Default in geom_smooth() is span = 0.75. This may not be the best choice for your specific dataset.

# smaller span values make the fit more wiggly, larger span values make it more smooth.

ggplot(mtcars) +

aes(disp, mpg) +

geom_point() +

geom_smooth(span = 0.25)`geom_smooth()` using method = 'loess' and formula = 'y ~ x'

ggplot(mtcars) +

aes(disp, mpg) +

geom_point() +

geom_smooth(span = 1)`geom_smooth()` using method = 'loess' and formula = 'y ~ x'

ggplot(mtcars) +

aes(disp, mpg) +

geom_point() +

geom_smooth(span = 2)`geom_smooth()` using method = 'loess' and formula = 'y ~ x'

For datasets with more than 1000 points, geom_smooth() uses a generalized additive model (GAM) with formula y ~ s(x, bs = "cs"). We can choose these settings manually by specifying the method and formula parameters:

ggplot(mtcars) +

aes(disp, mpg) +

geom_point() +

geom_smooth(method = "gam", formula = y ~ s(x, bs = "cs"))

GAMs fit splines to the data, and there is a wide array of different types of splines and spline settings (such as number of knots) that you can explore. For example, bs = "cs" specifies cubic regression splines with shrinkage. In the following, I will show a few more examples. Enter ?mgcv::smooth.terms in your R console to see the full documentation of available options.

ggplot(mtcars) +

aes(disp, mpg) +

geom_point() +

geom_smooth(

method = "gam",

# cubic spline with five knots

formula = y ~ s(x, k = 5, bs = 'cr')

)

ggplot(mtcars) +

aes(disp, mpg) +

geom_point() +

geom_smooth(

method = "gam",

# thin plate spline, three knots

formula = y ~ s(x, k = 3)

)

ggplot(mtcars) +

aes(disp, mpg) +

geom_point() +

geom_smooth(

method = "gam",

# Gaussian process spline, six knots

formula = y ~ s(x, k = 6, bs = 'gp')

)

Exercises

Explore the different smoothing options for the cars93 dataset. Pay particular attention to the behavior of the smoothing line on the right end of the data range, where the number of available points is sparse.

cars93 <- read_csv(

"https://wilkelab.org/SDS375/datasets/cars93.csv",

show_col_types = FALSE

)

ggplot(cars93) +

aes(x = Price, y = Fuel.tank.capacity) +

geom_point() + theme_bw(14) +

geom_smooth()`geom_smooth()` using method = 'loess' and formula = 'y ~ x'

# your code here